Table of Contents

- Why Crypto Holders Are Looking for Bank-Level Services

- What Defines a “Bank-Level” Crypto Platform in 2026

- Clapp: Licensed Infrastructure With Integrated Financial Tools

- Savings Products: Predictable Yield With Full Transparency

- Flexible Savings: Daily Liquidity With Daily Interest

- Fixed Savings: Locked Rates for Defined Terms

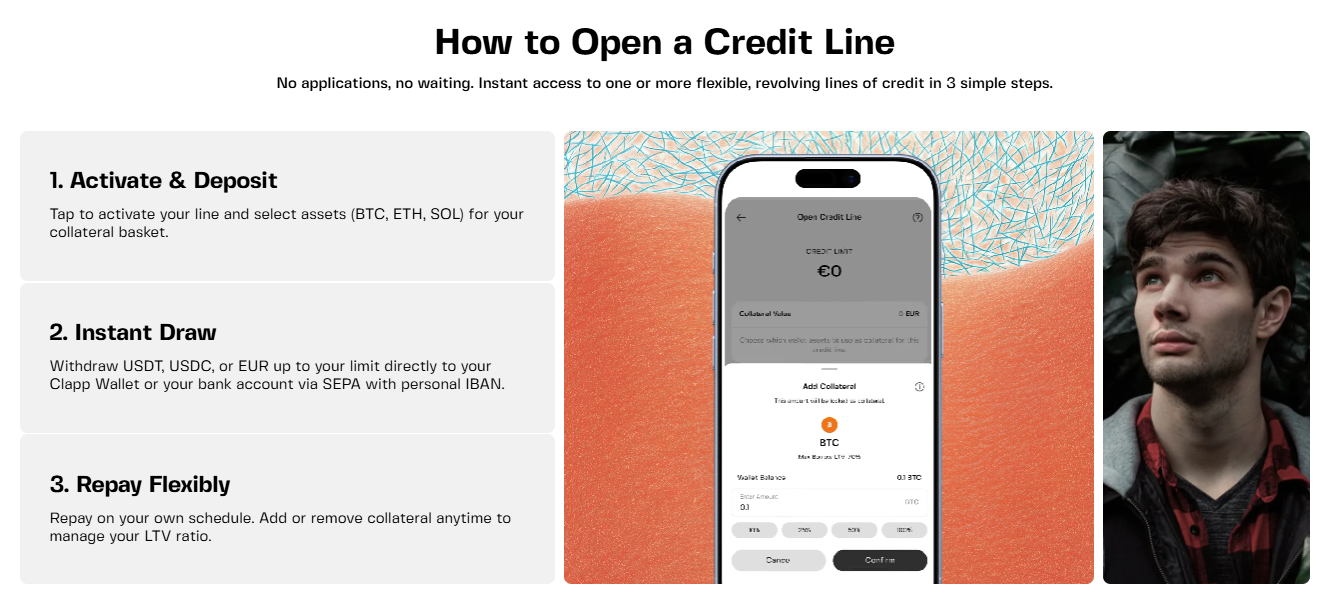

- Credit Lines: Liquidity Without Liquidation

- Fiat Integration: Bridging Crypto and Everyday Finance

- Security and Custody: Institutional-Grade Infrastructure

- All-in-One Architecture: From Fragmentation to Integration

- How Clapp Fits Into the Broader Shift Toward Everyday Crypto Use

- Final Assessment