Table of Contents

- What a Crypto Loan Is

- Why People Use Crypto Loans in Latin America

- How to Get a Crypto Loan

- Account and Verification

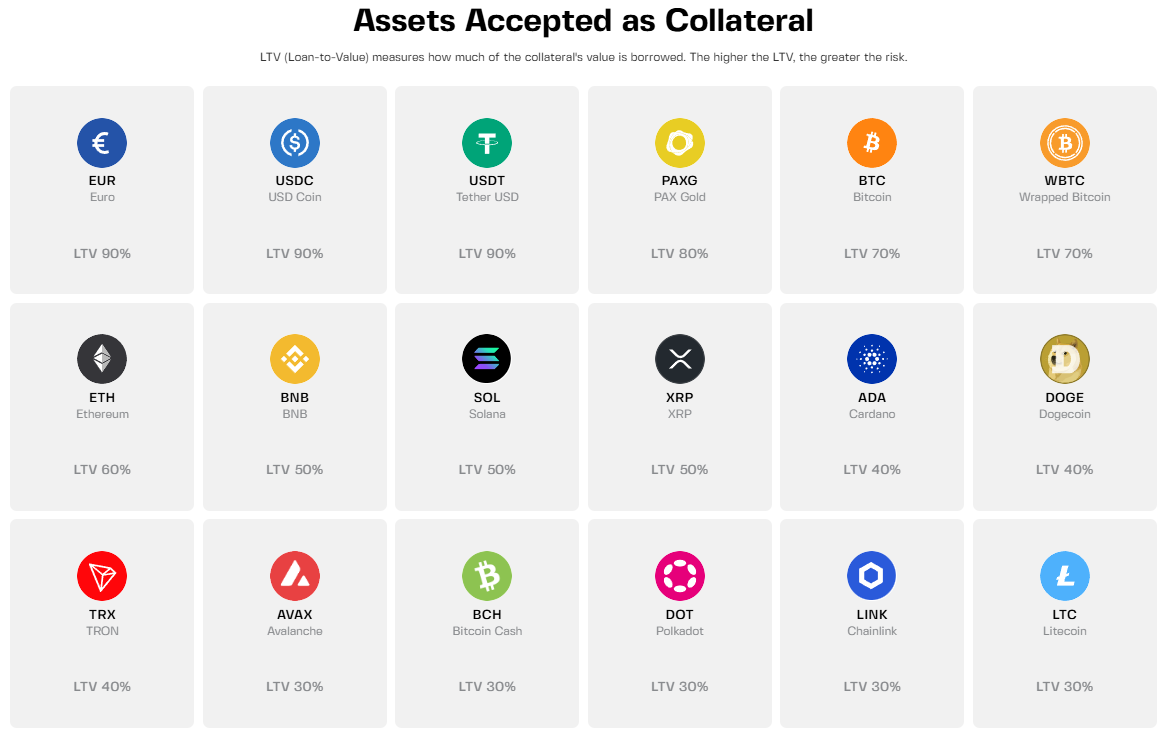

- Deposit Collateral

- Getting Access to Funds

- Withdrawing Funds

- A Simple Example

- Costs, Without Overcomplicating It

- Risk, Which Is Easy to Ignore at First

- Why Credit Lines Tend to Work Better Here

- Final Thoughts